Real Estate Loan Types: Which Loan Fits Which Property

An investor finds the right self-storage facility. Good location. Solid occupancy rate. Reasonable price. He calls his residential lender - the same one who did his last three rentals. Gets declined. Self-storage is commercial property, not residential. He scrambles to find a commercial lender. Closes six weeks late. Nearly loses the deal.

The whole problem: he assumed a mortgage is a mortgage.

The loan you use is not interchangeable. Different asset classes require different loan structures, different lenders, and different underwriting criteria. Calling the wrong lender doesn't just slow you down - it can kill a deal entirely.

This guide gives you the decision framework. Ten loan types. Sixteen asset classes. One map.

The Problem No One Tells You Until It's Too Late

Most real estate education treats loans as a footnote. Buy the property. Get a loan. Done. What kind of loan? Doesn't matter.

It does matter.

Loan type is determined by four things: the property type, the intended use, your borrower profile, and the deal structure. Change any one of those, and the right loan changes with it.

The wrong match creates real problems. Denied applications after weeks of underwriting. Wrong qualifying criteria - the lender asks for your personal tax returns when the deal needed to be underwritten on the property's income. Failed closings. Deals that die because the financing structure was never right for the asset.

Lenders specialize. A residential lender who does great work on single-family rentals probably doesn't touch mobile home parks. A commercial lender who knows apartment buildings may have no appetite for a billboard. Calling the wrong one doesn't just waste a phone call - it wastes weeks.

This post is also the financing primer for a 16-week asset class deep-dive series. Each upcoming post goes deep on one asset class: the market fundamentals, the metrics that matter, and the financing structure that fits. Keep this one bookmarked.

If you're modeling a specific deal right now, our buy property calculator lets you run the numbers before you call a lender.

A Quick Map of the Loan Landscape

Before getting into individual loan types, it helps to understand the three buckets. Once you know which bucket applies, you know which half of the loan products to ignore.

Bucket 1 - Residential / Government-Backed

These loans underwrite you: your income, your credit score, your debt-to-income ratio. The property matters, but the borrower is the primary risk factor.

Loan types in this bucket: Conventional, FHA, VA, USDA.

Bucket 2 - Income-Based

These loans underwrite the property: its ability to generate income that covers the debt payment. Your personal income, DTI, and number of other financed properties matter much less or not at all.

Loan types in this bucket: DSCR loans, Portfolio loans.

Bucket 3 - Bridge / Tactical

These loans underwrite the deal: the exit strategy, the timeline, the equity in the asset. They're short-term tools for specific situations - value-add plays, fast closings, transitional assets.

Loan types in this bucket: Bridge loans, Hard money, Commercial mortgages, Jumbo loans.

If you qualify on one bucket's criteria but not another, that tells you immediately which loan types to pursue - and which lenders to stop calling.

The Ten Loan Types

One section per loan type. Each covers what it is, who qualifies, which asset classes it fits, and the catch.

Conventional Loans

What it is: A standard conforming mortgage backed by Fannie Mae or Freddie Mac. Underwrites your personal income and credit history.

Who qualifies: W-2 income earners with good credit (620+ minimum, 720+ for best rates) and sufficient debt-to-income room.

Works for: Single-family rentals (1-4 units), primary residences, vacation homes.

Investment property rules: 15-25% down required. Expect a rate premium of 0.5-0.75% above what you'd pay on a primary residence.

The catch: Fannie Mae caps you at 10 financed properties. Once you hit that wall, conventional lending stops being an option. And as your portfolio grows, your DTI becomes harder to manage - each new property adds debt without adding qualifying income fast enough.

FHA Loans

What it is: A government-backed loan insured by the Federal Housing Administration. Lower barrier to entry, but comes with mortgage insurance premiums - 1.75% upfront, plus an annual MIP that continues for the life of the loan (or 11 years if LTV is 90% or below at origination).

Who qualifies: 3.5% down with a 580+ credit score. 10% down if your score is 500-579.

Works for: Primary residences - including house hacking. Buy a 2-4 unit property with FHA financing, live in one unit, rent the others. The rental income from the other units can offset a significant portion of your mortgage payment, and you get in at 3.5% down.

The catch: You must occupy the property. This is not a standalone rental play. MIP adds real long-term cost and affects your property's debt coverage numbers. See DSCR Explained if you want to understand how MIP affects cash flow math.

VA Loans

What it is: A loan benefit for eligible veterans, active service members, and surviving spouses. No down payment required. No private mortgage insurance.

Who qualifies: Requires a VA Certificate of Eligibility. A VA funding fee applies in most cases - 2.15% of the loan for first-time use with no down payment, 3.30% or more for subsequent use. Veterans with service-connected disabilities are exempt from the funding fee entirely.

Works for: Primary residences. The most powerful version of this for investors is the house hack: buy a 2-4 unit property with zero down, live in one unit, collect rent from the others. Zero down payment plus rental income offset is one of the lowest-cost entry points into real estate investing that exists.

The catch: Must occupy the property. Cannot use VA financing to purchase a standalone investment property you won't live in. NimbusPortfolio tracks VA loan details natively - including funding fee amounts and disability exemption status - so you don't have to manage that manually.

USDA Loans

What it is: A zero-down-payment, government-backed loan for properties in USDA-eligible rural and suburban areas.

Who qualifies: Income limits apply - typically at or below 115% of the area median income. The property must be located in a USDA-eligible area, which you verify by entering the specific parcel address on the USDA eligibility map.

Works for: Primary residences in rural or suburban markets. Some investors use USDA to get into a property in a rural market cheaply, house hack for the required occupancy period, then convert to a full rental.

The catch: Strictly primary residences. Geographic eligibility can change - a parcel that's eligible today may not be in a future USDA review cycle. Always verify the exact address before building your deal around USDA financing.

DSCR Loans (Debt Service Coverage Ratio Loans)

What it is: A non-QM loan that underwrites the property's income rather than your personal income. The property's rent relative to its debt payment determines whether you qualify - not your W-2, not your DTI, not how many other properties you own.

Who qualifies: Properties with a DSCR of 1.0 to 1.25 or higher, depending on the lender. Your employment status, income history, and number of financed properties don't factor in.

Works for: Single-family rentals, small multifamily (2-4 units), some 5+ unit properties, short-term rentals (when the lender accepts STR rental income - some use AirDNA projections, others require 12-month trailing history).

The catch: Rates run 0.5-1.5% higher than conventional. The property must be income-producing. Won't work for vacant land, development sites, or properties not generating rental income. This is the loan that breaks the DTI ceiling as your portfolio scales.

If you're not sure whether a property qualifies on income alone, start with the DSCR breakdown.

Wondering if a specific property qualifies on income alone? Run the numbers with our buy property calculator - it shows projected cash flow, estimated DSCR, and what loan structures could work.

Portfolio Loans

What it is: Loans originated and held by the lender rather than sold to Fannie Mae or Freddie Mac. Because the lender keeps it on their own books, they set their own rules. More flexible. Less standardized.

Who qualifies: Varies significantly by lender. Available to investors who've hit the conventional loan cap, or who own properties that don't meet Fannie/Freddie guidelines. Often requires an established lender relationship.

Works for: Small-to-mid multifamily, mixed-use properties, commercial real estate, non-warrantable condos, unusual property types that don't fit conventional boxes.

The catch: Terms vary widely. You can't comparison-shop these on rate aggregators - pricing requires direct lender conversations. Amortization is often shorter (15-20 years) and balloon payments (typically 5-10 years) are common. The lender relationship matters here more than any other loan type.

Commercial Mortgages

What it is: Financing for commercial real estate - broadly defined as properties with 5 or more residential units, or any property with a commercial use (office, retail, industrial, warehouse, self-storage, mixed-use). Completely separate underwriting world from residential.

Who qualifies: Underwritten primarily on the property's net operating income and DSCR (1.25+ is a common minimum). The lender will also look at your net worth and prior experience with commercial assets. Personal income matters, but less than it does in residential underwriting.

Works for: Apartment buildings (5+ units), office buildings, retail, industrial, warehouse, mixed-use, self-storage facilities, mobile home parks.

Key differences from residential: Shorter amortization (20-25 years is common). Balloon payments (30-year amortization with a 10-year balloon is a standard structure). 25-35% down required. Lenders require full rent rolls and operating statements, not just tax returns.

One note on SBA: the SBA 7(a) and SBA 504 programs exist for owner-occupied commercial real estate. SBA 504 in particular allows 10% down for business owners buying the building their business operates in - a different use case from investment, but worth knowing.

Bridge Loans

What it is: Short-term financing (6 to 36 months) that bridges the gap between purchase and permanent financing. Used during renovation, stabilization, or situations where speed matters more than rate.

Who qualifies: More asset-based than income-based. The property's value and equity position matter more than your personal income. Creditworthiness still factors in, but the lender's primary question is whether your exit strategy makes sense.

Works for: Value-add plays, the BRRRR strategy, properties transitioning between uses, assets not yet stabilized enough for permanent financing.

The catch: High rate - typically prime plus 2-4%, often interest-only. Short term. If you can't refinance or sell when the term expires, you have a real problem. The exit strategy isn't just important - it's everything.

Hard Money Loans

What it is: Short-term, asset-based financing from private lenders. Fastest to close (7-14 days is realistic). Highest cost. Qualification is based almost entirely on the property's loan-to-value ratio, not the borrower's creditworthiness.

Who qualifies: Almost anyone with sufficient equity in the deal and a clear exit strategy. Credit matters far less than deal quality.

Works for: Fix-and-flip projects, distressed acquisitions, auction purchases, any situation where speed matters more than rate.

The catch: Rates of 10-14%+ are normal. Origination fees (points) of 2-4% are standard. These are transactional tools - they are not hold-forever financing.

Hard money and bridge loans are often used interchangeably, but they're not identical. Hard money is typically shorter-term, higher-cost, and purely asset-focused. Bridge loans can be institutional with better terms and longer windows. The distinction matters when you're modeling your exit.

Jumbo Loans

What it is: A residential mortgage that exceeds the conforming loan limit set by the FHFA - $806,500 in most U.S. markets in 2026, with higher limits in designated high-cost areas. Lenders hold these on their own books because they can't be sold to Fannie or Freddie.

Who qualifies: Strong income, 720+ credit score typically required, substantial liquid assets, low DTI. Underwriting is more rigorous than conforming loans.

Works for: High-value single-family homes, luxury properties, high-cost coastal and mountain markets.

The catch: Stricter underwriting and a rate premium above conforming. Investor property jumbos exist but are even more restrictive. If you're buying a $1.5M short-term rental cabin in a resort market, a jumbo is likely the structure you're working with.

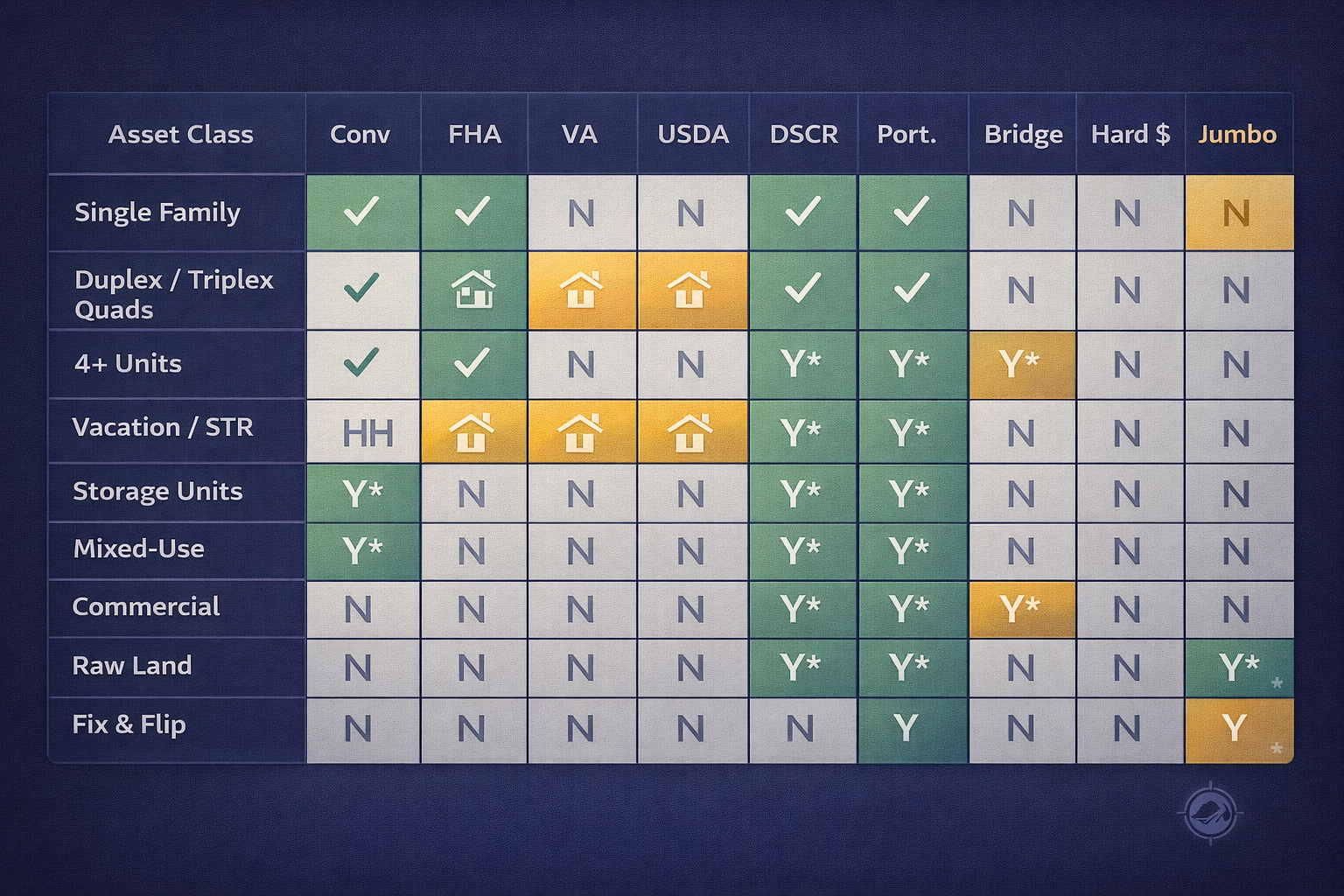

The Decision Matrix

Keep this reference. When you're evaluating any new deal, start here - it tells you which loan types are worth pursuing and which lenders to stop calling.

Legend:

- ✓ = Standard use case

- ✓* = Yes, with conditions or lender-specific requirements

- HH = Yes for house hacking (must occupy one unit)

- ** - ** = Not the right tool for this asset class

Lender overlays and property-specific factors always apply. This table is a starting point, not a final answer. The asterisks mark situations where some lenders participate and others won't - which is why finding a lender who specializes in that specific asset class matters. A generalist lender will often decline the same deal that a specialist closes without hesitation.

Four Scenarios That Show How This Works

Investors don't shop loan types in the abstract. They're looking at a specific deal with specific constraints. Here's the matrix in practice.

Scenario 1 - The House Hacker Starting Out

Profile: W-2 income, solid credit, limited cash reserves.

Property: 3-unit building, $320,000 purchase price in a mid-size market.

Right loan: FHA at 3.5% down ($11,200) - or VA at zero down if eligible.

Why it works: Owner-occupancy satisfies the FHA requirement. Rental income from the other two units offsets most of the mortgage. Low down payment preserves capital for reserves and future deals.

The move after year 1-2: Once the property stabilizes and you move out, refinance to a conventional or DSCR loan and repeat the process with a new property.

Scenario 2 - The Experienced Investor Hitting the Fannie Cap

Profile: Owns 10 properties, all financed conventionally. Hit the Fannie Mae limit. Has a solid track record but can't get another conventional loan.

Property: A duplex at $280,000 in a strong rental market, projected DSCR of 1.30.

Right loan: DSCR loan - the property's income qualifies it, not the investor's personal DTI.

Why it works: DSCR lenders don't count how many financed properties you have. They care about whether the property pays for itself. A 1.30 DSCR is comfortably above most lenders' minimums.

If you're not sure whether the property clears the bar, start with the DSCR breakdown.

Scenario 3 - The Value-Add Commercial Play

Profile: Experienced investor moving from residential into commercial, buying a 12-unit apartment building.

Property: 12 units, 7 occupied (58% occupancy), $1.2M purchase price. Needs light renovation and new management.

Right loan: Bridge loan to close and stabilize - then refinance to a permanent commercial mortgage once occupancy reaches 85-90%+.

Why it works: At 58% occupancy, the property doesn't generate enough NOI to qualify for permanent commercial financing. A bridge loan gets you in the door. Stabilization gets you the permanent loan at better terms.

What to watch: The bridge term (12-24 months is typical), the exit rate you'll qualify for on the commercial refinance, and whether your renovation budget and lease-up timeline are realistic.

Modeling the refinance from bridge to permanent? Our refinance calculator shows your new payment, break-even, and whether the numbers work. We also wrote a full guide on when to refinance - worth reading before you call a lender.

Scenario 4 - The Self-Employed STR Buyer

Profile: Self-employed, variable income, buying an STR cabin in a mountain resort market.

Property: $650,000 cabin with projected STR revenue of $72,000/year.

Right loan: DSCR loan using STR income. Some lenders accept AirDNA revenue projections; others require 12 months of trailing rental history.

Why it works: DTI qualification on a conventional loan is difficult when income is variable. A DSCR loan sidesteps personal income entirely - the lender cares whether $72,000/year covers the debt service, not whether your 2025 Schedule C looks right.

The catch: Not all DSCR lenders accept STR income. Some require the property to be a long-term rental. Find a lender who specifically advertises STR DSCR experience - the product exists, but it's not universal.

The Most Common Mismatch Questions

Can I use a conventional loan for a mobile home park?

No. Mobile home parks are commercial real estate. You need a commercial mortgage or a portfolio lender. Calling a residential lender for this costs you weeks, not days.

Can I use a VA loan for a rental property I won't live in?

No - not unless you're house hacking. VA loans require owner-occupancy. If a lender suggests otherwise, find a different lender.

Is a DSCR loan the same as a hard money loan?

No. DSCR loans are long-term permanent financing - typically 30-year terms. Hard money is short-term (6-24 months), high-cost, and built for transactions, not holds. The names sound similar. The use cases are completely different.

Is a duplex commercial property?

No. Properties up to 4 units are residential under conventional and FHA definitions. Five units and above crosses into commercial underwriting. That line at 4-to-5 units matters a lot when you're choosing a lender.

What Comes Next in This Series

This post is the financing primer for a 16-week asset class series. Each upcoming post goes deep on one asset class - the market fundamentals, the performance metrics that matter, and the financing structure that fits.

Upcoming deep dives: single-family rentals, short-term rentals, small multifamily, self-storage, mobile home parks, agricultural land, commercial real estate, and specialty assets including billboards, cell towers, and mineral royalties. Bookmark this financing guide and come back to it as each post drops - the loan type section for each asset class will make more sense with this foundation in place.

Start building the knowledge base now:

- DSCR: The one metric that tells you if your property can pay for itself

- When to refinance - and when not to

- Leverage: How much of your portfolio you actually own

- Total return on equity: Beyond cash flow

- Why your billboard and duplex don't belong in the same spreadsheet

How Nimbus Tracks Loan Details Across Your Portfolio

Once you have multiple properties across multiple loan types - conventional on the SFR, DSCR on the duplex, commercial mortgage on the apartment, bridge loan on the storage facility - tracking all of it in a spreadsheet becomes a second job. Different terms. Different amortization schedules. Different balloon payment dates. Different MIP schedules if you have FHA loans in the mix.

NimbusPortfolio tracks loan details for every property in one place: amortization schedules, VA funding fee records, FHA MIP schedules, balloon payment dates, DSCR by property, and remaining loan balance across the full portfolio. When you're evaluating whether to refinance one property, you can see the current balance, rate, and remaining term without rebuilding a spreadsheet from scratch.

The platform supports 19+ asset types - including commercial, self-storage, mobile home parks, and specialty assets - so your loan tracking doesn't stop at the residential side of your portfolio.

Start your free trial - no credit card required. Track every loan across every asset type in one view.

The Bottom Line

The loan type is not a minor detail. It is the structure everything else sits on. The wrong structure for the asset class means the wrong lender, wrong underwriting criteria, wrong terms - or no deal at all.

Use the matrix. Start with the asset type. Match the loan type to the property's income characteristics and your borrower profile. Then find lenders who specialize in that specific product for that specific asset class. A specialist who does ten DSCR loans a month will close your deal. A generalist who does one a year probably won't.

You don't need to memorize every loan product. You need to know which bucket applies - residential, income-based, or tactical - and which products live in that bucket. The rest is a lender conversation.

The investors who move fastest aren't the ones who know the most. They're the ones who ask the right question first.