Beyond Cash Flow: Understanding Your Total Return on Equity

You bought a property for $300,000 ten years ago. Today it's worth $650,000.

The monthly rent checks arrive like clockwork. Your accountant nods approvingly. Your family calls it your "retirement property."

But here's the question most investors never ask:

What is your equity actually earning?

Not your cash flow. Not your appreciation. Your complete, total return on the $500,000 of equity you have sitting in that property.

Because once you know that number, you can make an informed decision about whether that's the best place for your money to be working.

The Number Most Investors Calculate Wrong

Ask ten real estate investors "What's your return on equity?" and you'll get ten different answers.

Some will quote their cash-on-cash return from purchase (irrelevant now).

Some will cite their cap rate (useful, but incomplete).

Some will just talk about cash flow dollars (missing the bigger picture).

Almost none will give you their total return on equity - which is the only number that actually matters when deciding what to do with that equity.

Here's why: Your property generates returns in two distinct ways.

1. Cash Flow (liquid, spendable, in your pocket)

2. Equity Growth (illiquid, building wealth, on paper)

Both are real returns. Both are valuable. But they serve different purposes in your financial life.

Let's Run the Real Numbers

Your property today:

- Current market value: $650,000

- Remaining mortgage: $150,000

- Your equity: $500,000

- Annual net cash flow: $18,000

One year later:

- Property appreciated 3%: Now worth $669,500

- Principal paid down: Mortgage now $142,500

- Your equity: $527,000

- Annual cash flow: $18,000

What just happened:

You received $18,000 in cash (3.6% of your equity).

Your equity grew by $27,000 (5.4% of your equity).

Total return: $45,000 on $500,000 = 9% ROE

That's not bad. That's actually competitive with long-term stock market returns, without the volatility, and you own a tangible asset.

But here's where it gets interesting: Only $18,000 of that $45,000 is liquid.

The Liquidity vs. Total Return Trade-Off

This is where most discussions about equity deployment go wrong.

They treat 9% like it's a disappointment. They compare it to S&P 500 historical averages (15.91%) and conclude you should sell everything and buy index funds.

But that comparison ignores reality:

Real Estate 9% Return:

- 3.6% liquid cash you can spend

- 5.4% equity growth building wealth

- Zero volatility in the income stream

- Tangible asset you control

- Tax advantages (depreciation, interest deductions)

- No sequence-of-returns risk

Stock Market 15.91% Historical Return:

- 100% illiquid until you sell (then you pay taxes)

- Includes -18% years like 2022

- Requires perfect behavior during crashes

- Zero control over the asset

- Dividends are taxable

- Sequence-of-returns risk is real

Neither is better or worse. They're different tools for different jobs.

When Your Equity Should Move

So if 9% total return is solid, when DOES it make sense to redeploy equity?

You should consider redeployment when:

-

The full return (cash flow + equity growth) is genuinely low

- Sub-6% total return after accounting for everything

- Alternative opportunities offer materially better risk-adjusted returns

- Transaction costs won't eat your gains

-

You need liquidity more than you need equity growth

- Emergency fund is too small

- Better opportunities require liquid capital NOW

- Life circumstances have changed

-

You can deploy into more real estate at better numbers

- Current property: 9% total return

- Available properties: 12-15% total return on fresh equity

- Transaction costs are worth the upgrade

-

You're over-concentrated in one asset or market

- Single property represents 70%+ of net worth

- Geographic concentration creates unacceptable risk

- Diversification provides real risk reduction

You should probably hold when:

-

Transaction costs are too high

- Capital gains tax: 15-20% federal + state

- Depreciation recapture: 25%

- Real estate commission: 5-6%

- These can consume 30-40% of your equity before redeployment

-

You locked in a valuable low rate

- 3% mortgage when current rates are 7%

- Interest rate savings may exceed alternative returns

- Refinancing to extract equity destroys this advantage

-

Your total return is competitive

- 8-10% total ROE is solid

- Alternative opportunities aren't materially better after taxes

- The known quantity has value

-

You value simplicity

- Current setup works and doesn't stress you

- More properties = more management time

- Stocks require emotional discipline you might not have

The Three Deployment Options

If you've decided your equity should move, you have three paths:

Option A: Keep It (The Preservation Strategy)

When this makes sense:

- Your total ROE is 8%+

- You have a low interest rate worth preserving

- Transaction costs would eat too much equity

- You prefer simplicity and known quantities

- The property fits your long-term strategy

The math:

- 9% total return on $500k equity = $45,000/year

- $18,000 liquid cash flow

- $27,000 building wealth through equity growth

- Zero transaction costs

- Zero added complexity

Option B: Deploy Into Index Funds (The Liquidity Strategy)

When this makes sense:

- You want 100% liquidity

- You can emotionally handle market volatility

- You don't want to manage properties

- Your total ROE is below 7%

- You have a long time horizon (10+ years)

The HELOC approach:

- Keep the property AND the low rate

- Open a HELOC to access equity

- Deploy borrowed capital into index funds

- Preserve real estate position while adding liquidity

Example math:

- $150,000 HELOC at 8% interest = $12,000/year cost

- S&P 500 historical return (15.91%) = $23,865/year

- Net gain: $11,865/year from HELOC deployment

- Plus you keep property's $18,000 cash flow

- Total: $29,865/year vs. $18,000 (but at higher risk)

Critical considerations:

- HELOC interest typically NOT deductible for investments

- Market volatility can be stomach-churning (-18% years happen)

- You're carrying debt against a volatile asset

- Behavioral challenge: Can you hold through crashes?

- 2008, 2020, 2022 remind us that drawdowns are real

Option C: Deploy Into More Real Estate (The Multiplication Strategy)

When this makes sense:

- You love real estate and have systems in place

- Current property's total ROE is below 8%

- You can find properties with 10-12%+ total ROE potential

- You have time for management (or budget for PM)

- You want tax advantages and tangible assets

Three sub-strategies:

1. HELOC method (keep property, use equity for new purchases)

- Preserve current property and low rate

- Use equity as down payments on new properties

- HELOC interest IS deductible for rental purchases

- Maintain control and tax advantages

2. 1031 Exchange

- Sell property tax-deferred

- Redeploy entire equity amount

- Reset depreciation schedules

- Strict IRS timelines (45/180 days)

3. Cash sale

- Sell property, pay capital gains

- Redeploy after taxes

- No timeline pressure

- Most flexibility, highest immediate tax cost

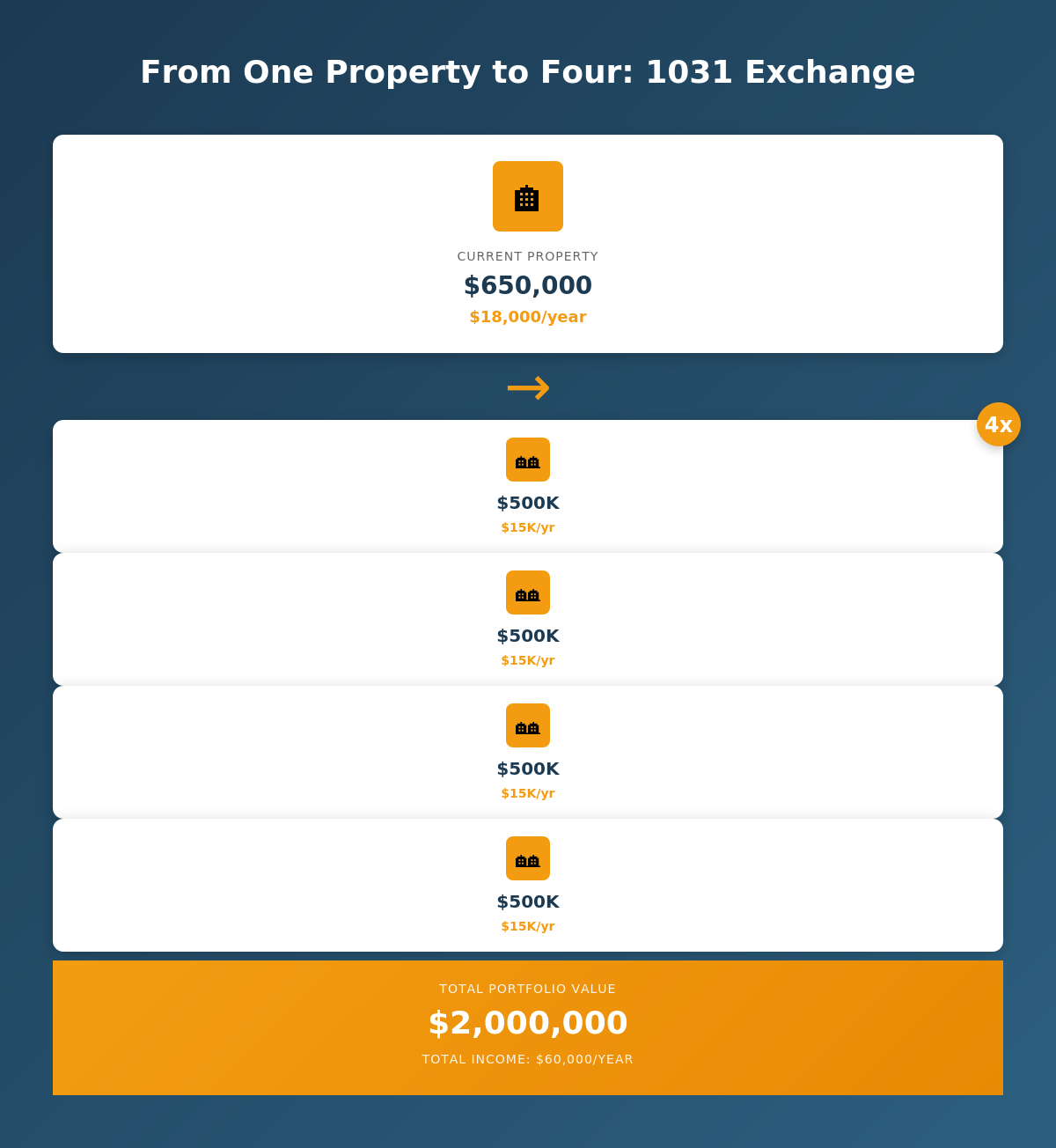

Example math (1031 Exchange):

- $500,000 equity after tax-deferred sale

- Deploy as 25% down payment across 4 properties

- Total portfolio value: $2,000,000

- If each property generates $15,000/year cash flow

- Total cash flow: $60,000/year vs. original $18,000/year

- Plus continued appreciation and principal paydown across 4 assets

The trade-offs:

- 4x the tenant relationships

- 4x the maintenance calls

- 4x the vacancy risk

- Significant time commitment increase

- Geographic concentration risk (unless investing nationally)

- Tax advantages: New depreciation schedules, deductible interest

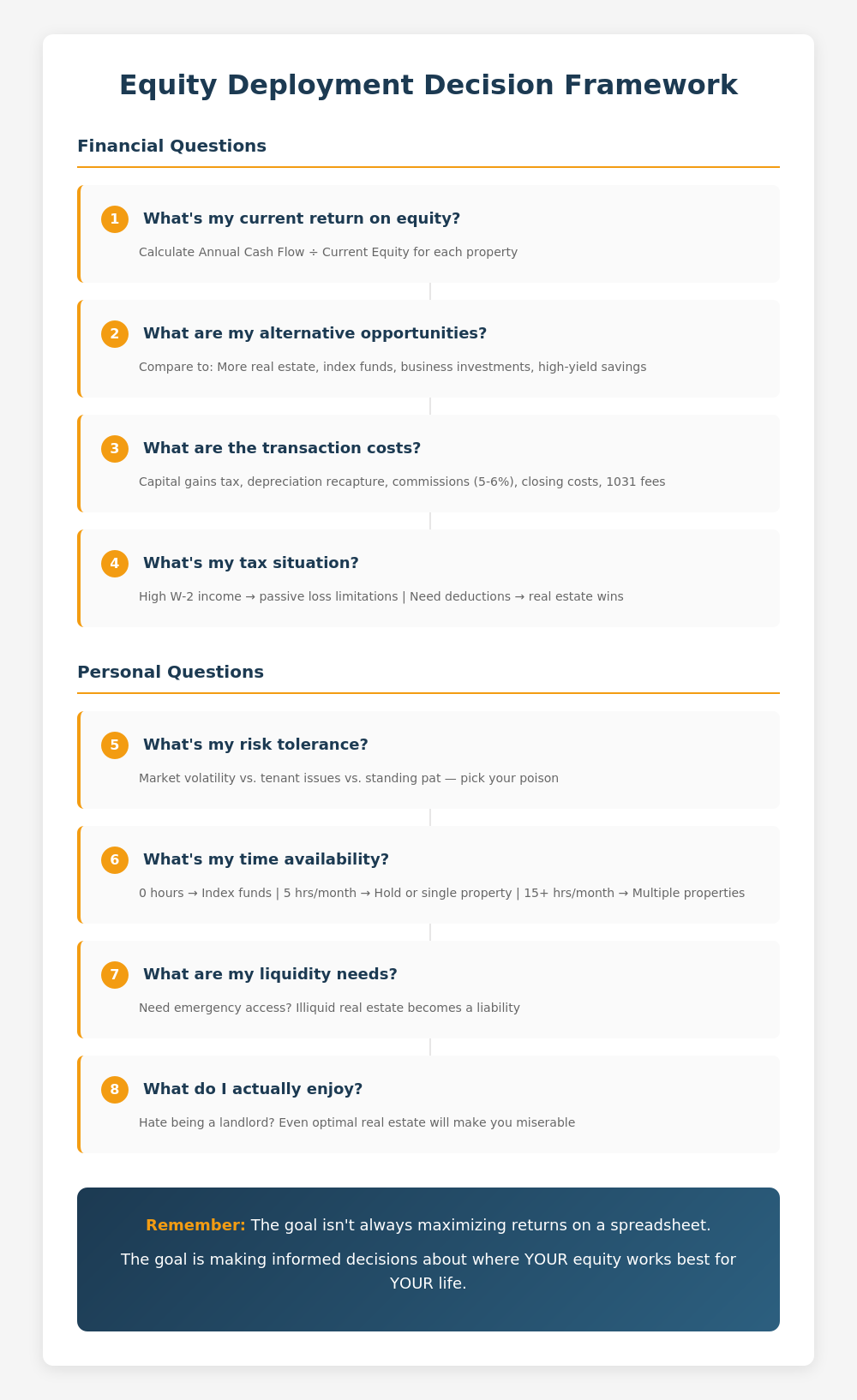

The Real Decision Framework

Forget the spreadsheets for a moment. Here are the questions that actually matter:

Financial Questions

1. What's my TOTAL return on equity?

- (Cash Flow + Equity Growth) / Current Equity

- Not just cash flow - the complete picture

- Calculate this for every property you own

2. What can I earn elsewhere, AFTER all costs?

- Index funds: Historical returns - volatility risk - behavioral risk

- More real estate: New property returns - transaction costs - time cost

- Don't compare gross numbers to gross numbers

3. What are my transaction costs, really?

- Capital gains tax calculator (federal + your state)

- Depreciation recapture (25% on total depreciation taken)

- Real estate commission (5-6% of sale price)

- Closing costs, 1031 intermediary fees

- Add it all up before you assume redeployment makes sense

4. What's my tax situation?

- High W-2 income? Passive loss limitations may apply

- Need deductions? Real estate provides them

- Low tax bracket? Stocks might be more efficient

Personal Questions

5. What do I value more: cash flow or total return?

- Need cash today? That liquid 3.6% matters more

- Building wealth for later? Total 9% is what counts

- Both are valid - but they're different strategies

6. How much time do I actually have?

- 0 hours available → Index funds or hold current property

- 5 hours/month → Current property or single property management

- 15+ hours/month → Multiple properties or active management

7. What are my liquidity needs?

- Emergency fund adequate? Real estate is fine

- Need access to capital quickly? Illiquid real estate is a problem

- Uncertain future? Liquidity has option value

8. What do I actually enjoy?

- Love being a landlord? More real estate makes sense

- Hate tenant calls? Don't double down on properties

- Enjoy set-it-and-forget-it? Index funds might fit better

Three Real Examples

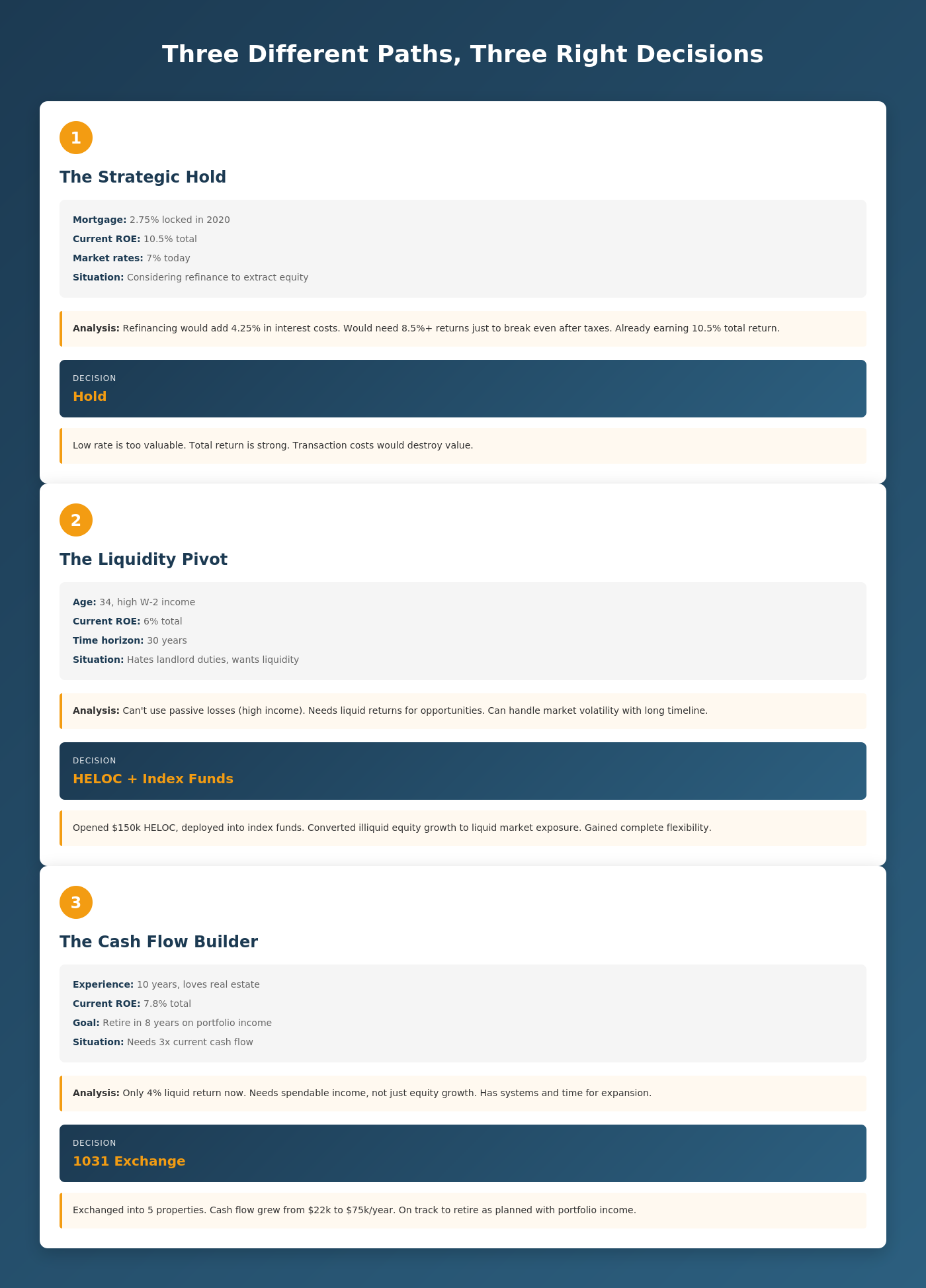

Case Study 1: The Smart Hold

Investor profile:

- 2.75% mortgage rate locked in 2020

- Property worth $550k, mortgage $250k, equity $300k

- Cash flow: $15,000/year (5% cash-on-cash)

- Equity growth: $16,500/year (3% appreciation)

- Total ROE: 10.5%

Alternative: Refinance to extract equity

- New rate would be 7% (4.25% increase)

- Additional $4,250/year in interest on $100k extraction

- Need to earn 8.5%+ after taxes just to break even

- Already earning 10.5% total return

Decision: Hold

The low rate is too valuable. Total return is solid. Transaction costs and rate increase would destroy value.

Case Study 2: The Liquidity Pivot

Investor profile:

- Age 34, high W-2 income ($180k/year)

- Property worth $400k, equity $280k

- Cash flow: $8,400/year (3% of equity)

- Equity growth: $8,400/year (3% appreciation)

- Total ROE: 6%

Concerns:

- Can't use passive losses (too much W-2 income)

- Hates dealing with tenants

- Wants liquidity for opportunities

- 30-year time horizon

- Comfortable with market volatility

Decision: HELOC + Index Funds

- Opened $150k HELOC at 7.5% ($11,250/year cost)

- Deployed into index funds

- Accepts volatility for liquidity

- Total ROE could improve to 9-10% depending on market

- Gains complete liquidity and simplicity

Case Study 3: The Real Estate Expansion

Investor profile:

- Experienced investor, 10 years active

- Property worth $700k, equity $550k

- Cash flow: $22,000/year (4% of equity)

- Equity growth: $21,000/year (3% appreciation)

- Total ROE: 7.8%

Opportunity:

- Found 4 properties in growth markets

- Each could generate $18,000/year cash flow

- Each priced at $450k (needs $112,500 down)

- Can 1031 exchange entire equity

Decision: 1031 Exchange

- Sold property tax-deferred

- Exchanged into 4 properties totaling $1.8M

- New total cash flow: $72,000/year (vs. $22,000)

- New total equity growth potential: $54,000/year (3% on $1.8M)

- New total ROE: 22.9% (on $550k deployed equity)

- Time commitment increased but within comfort zone

- Massive increase in depreciation deductions

The Uncomfortable Truth

Here's what no spreadsheet will tell you:

Sometimes the "right" financial move is the wrong life move.

The math might scream "1031 into 8 properties!" but if you're stressed and time-starved, that's a recipe for misery.

The math might say "HELOC into index funds!" but if you'll panic-sell during the next -20% year, you'll lock in losses and destroy returns.

The math might say "Your 9% return is fine, stop overthinking it!" but if you're deeply unsatisfied with your real estate concentration, that psychological cost is real.

What Actually Matters

Your equity is always working somewhere.

Right now, it's working in that property generating:

- Cash flow you can spend

- Equity growth you're building

- Stability and tangible assets

- Tax advantages and control

Maybe that's exactly where it should be - for YOUR situation, YOUR goals, YOUR life.

Or maybe it should be working somewhere else.

But you can't make that decision until you know:

- What your TOTAL return on equity actually is (not just cash flow)

- What alternatives exist after accounting for ALL costs

- What trade-offs matter to YOU beyond just returns

- What your life and goals actually look like

The goal isn't to always maximize returns on a spreadsheet.

The goal is to make informed decisions about where your equity works best for your life.

Sometimes that means holding because you value simplicity.

Sometimes that means stocks because you value liquidity.

Sometimes that means more real estate because you value control and tax benefits.

All three can be right. But they're only right when chosen consciously, with eyes wide open to the complete picture.

How Nimbus Portfolio Helps

At Nimbus Portfolio, we built tools specifically to answer these questions:

→ Total Return on Equity tracking - Cash flow + equity growth across your entire portfolio

→ Scenario modeling - Compare hold vs. sell vs. HELOC vs. 1031 before making moves

→ Tax impact projections - See actual costs of sales, exchanges, and HELOC strategies

→ Portfolio-level intelligence - Understand ALL your equity, not just individual properties

Because your equity isn't trapped. And it's not underperforming.

It's just waiting for you to understand its complete return - and make an informed decision about whether that's the best place for it to work.

Ready to see your complete return on equity across all your properties? Track your total portfolio intelligence →