Leverage: The Number That Shows How Much of Your Portfolio You Really Own

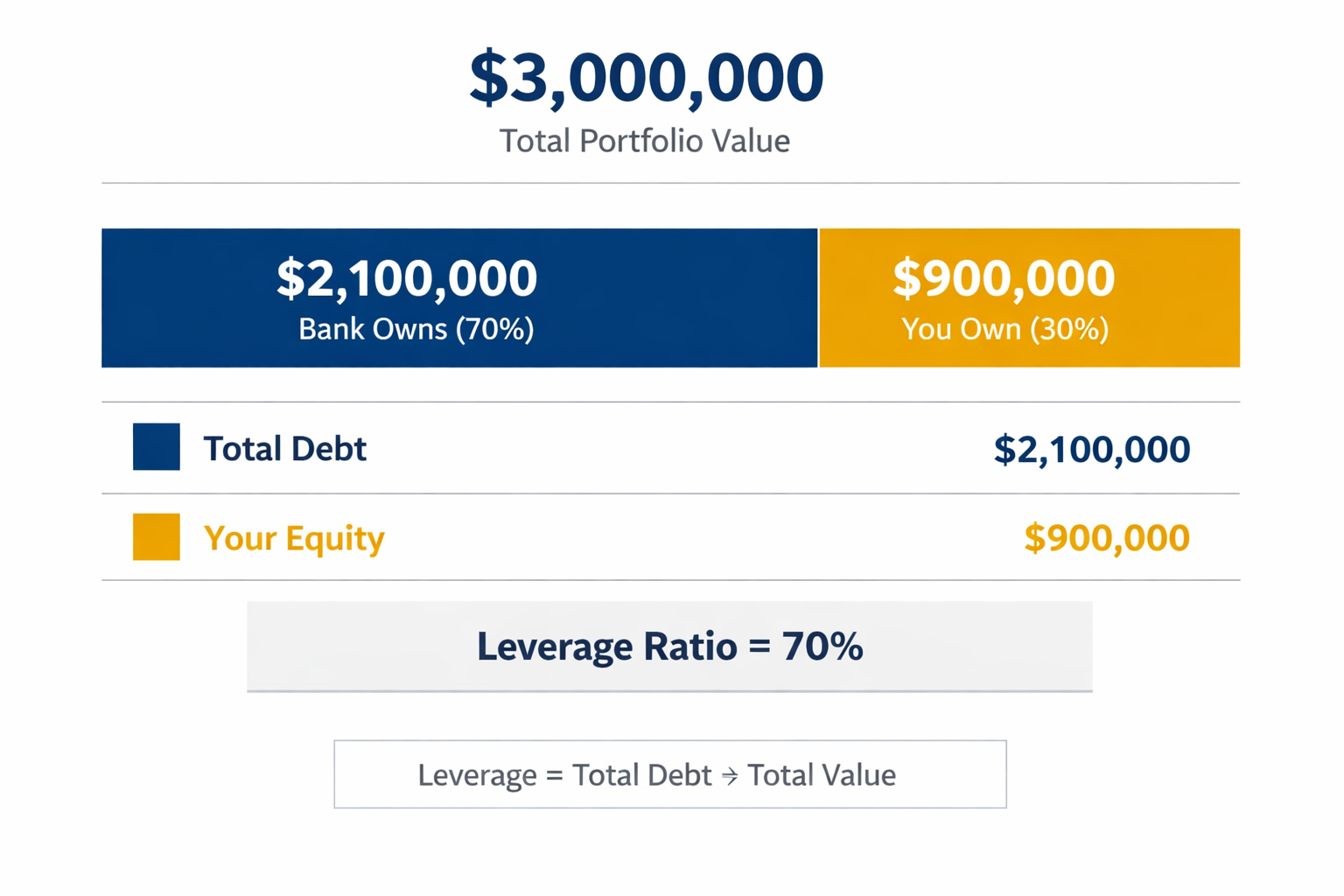

You own a $3 million real estate portfolio.

Impressive.

But here's the question nobody asks: How much of it do you actually own?

If your leverage is 70%, you own $900,000. The bank owns $2.1 million.

This isn't a judgment. It's just math. But it's math that changes everything about how you should think about risk, returns, and your next move.

What Leverage Actually Means

Leverage is simple:

Total Debt ÷ Total Value = Leverage Ratio

A $400,000 property with a $320,000 mortgage has 80% leverage.

Translation: You own 20%. The bank owns 80%.

Most investors know their loan-to-value ratio per property. Few know their portfolio-wide leverage. Even fewer understand what that number actually means for their wealth-building strategy.

Because leverage isn't just about risk. It's a multiplier that amplifies everything - the good, the bad, and the completely unexpected.

The Multiplier Effect Nobody Calculates

Here's where leverage gets interesting.

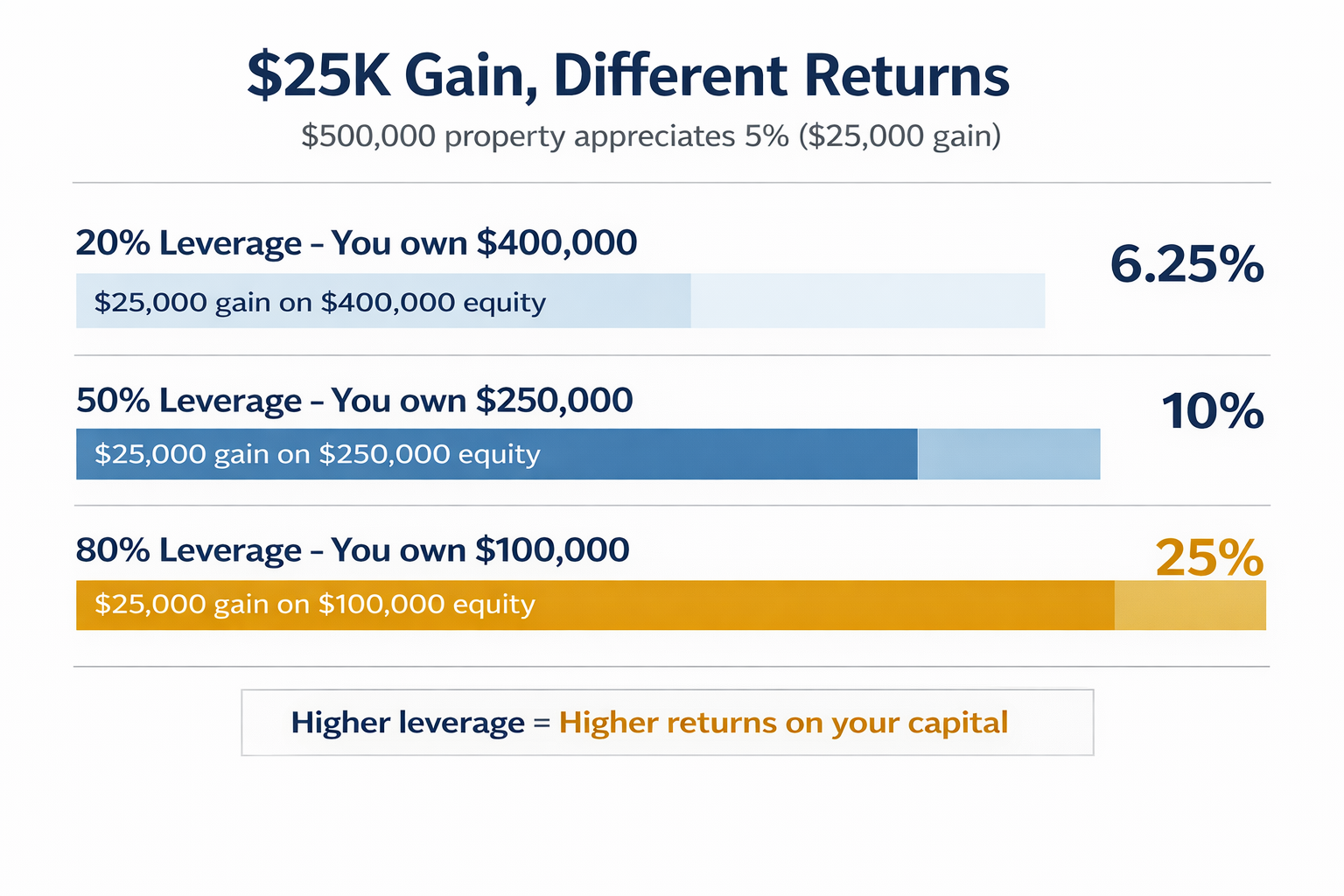

Take a $500,000 property that appreciates 5% in one year. That's a $25,000 gain.

But your return on equity depends entirely on how much you own:

Scenario A: 20% Leverage (You own $400k)

- $25,000 gain on $400,000 equity = 6.25% return

Scenario B: 50% Leverage (You own $250k)

- $25,000 gain on $250,000 equity = 10% return

Scenario C: 80% Leverage (You own $100k)

- $25,000 gain on $100,000 equity = 25% return

Same property. Same market. Same appreciation. Completely different outcomes.

This is why investors use leverage. A 25% return beats a 6.25% return every single time - as long as the property keeps appreciating.

And then what?

That's where second-order thinking comes in.

When The Multiplier Works Against You

Leverage doesn't care about your intentions. It just multiplies.

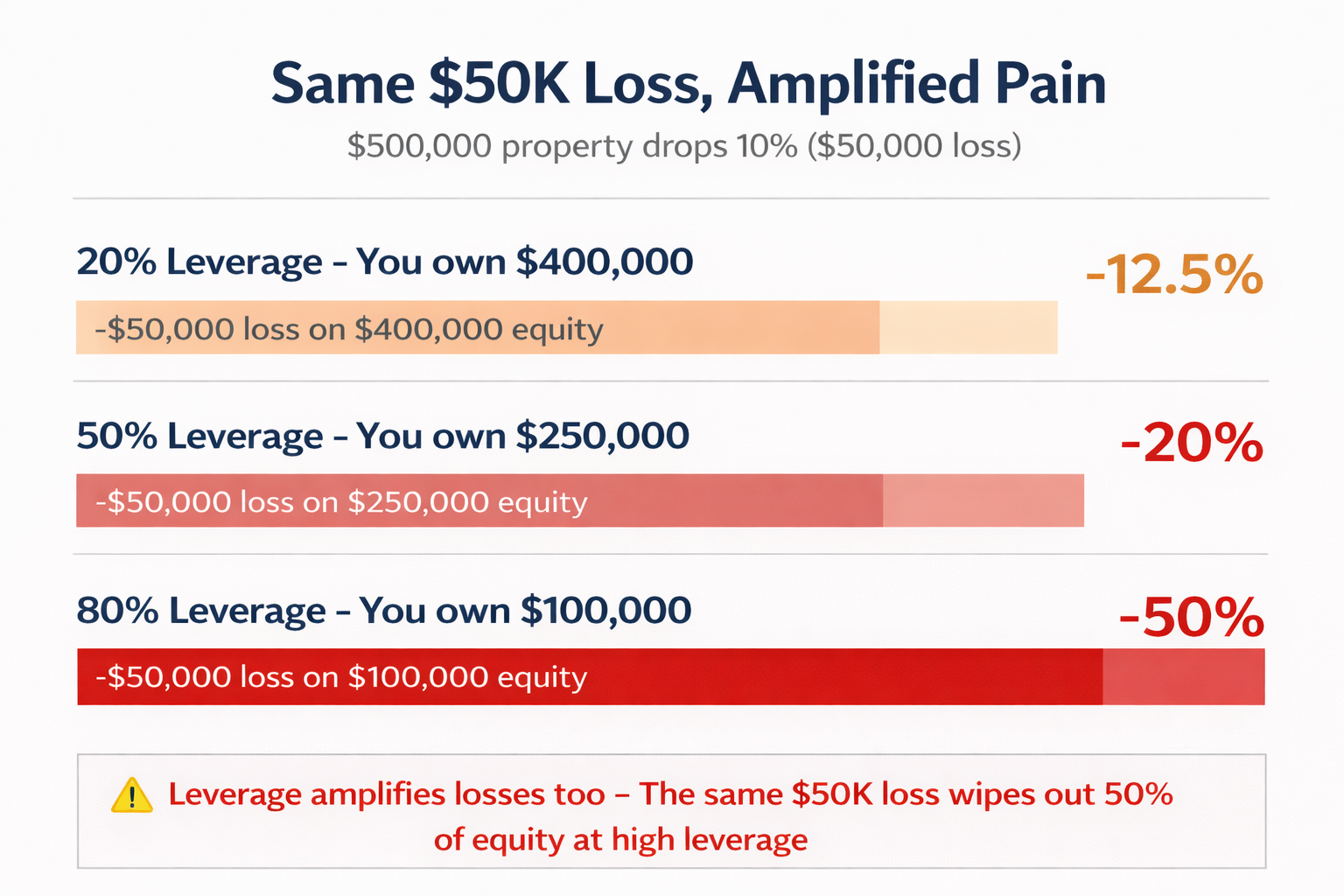

Same $500,000 property. But this time it drops 10% in value. You just lost $50,000.

Scenario A: 20% Leverage

- -$50,000 loss on $400,000 equity = -12.5%

Scenario B: 50% Leverage

- -$50,000 loss on $250,000 equity = -20%

Scenario C: 80% Leverage

- -$50,000 loss on $100,000 equity = -50%

Half your equity gone. Same property that would have been a -12.5% hit is now a -50% wipeout.

And then what?

If you're at 80% leverage and values drop 20%? You're at 100% LTV. Zero equity. The bank owns everything. If you need to sell, you're writing a check at closing.

This is what happened in 2008. High leverage + falling values + forced sales = complete wipeout.

The question isn't whether leverage is good or bad. It's whether you understand what you're amplifying.

The Number Most Investors Never Calculate

Here's what most investors do:

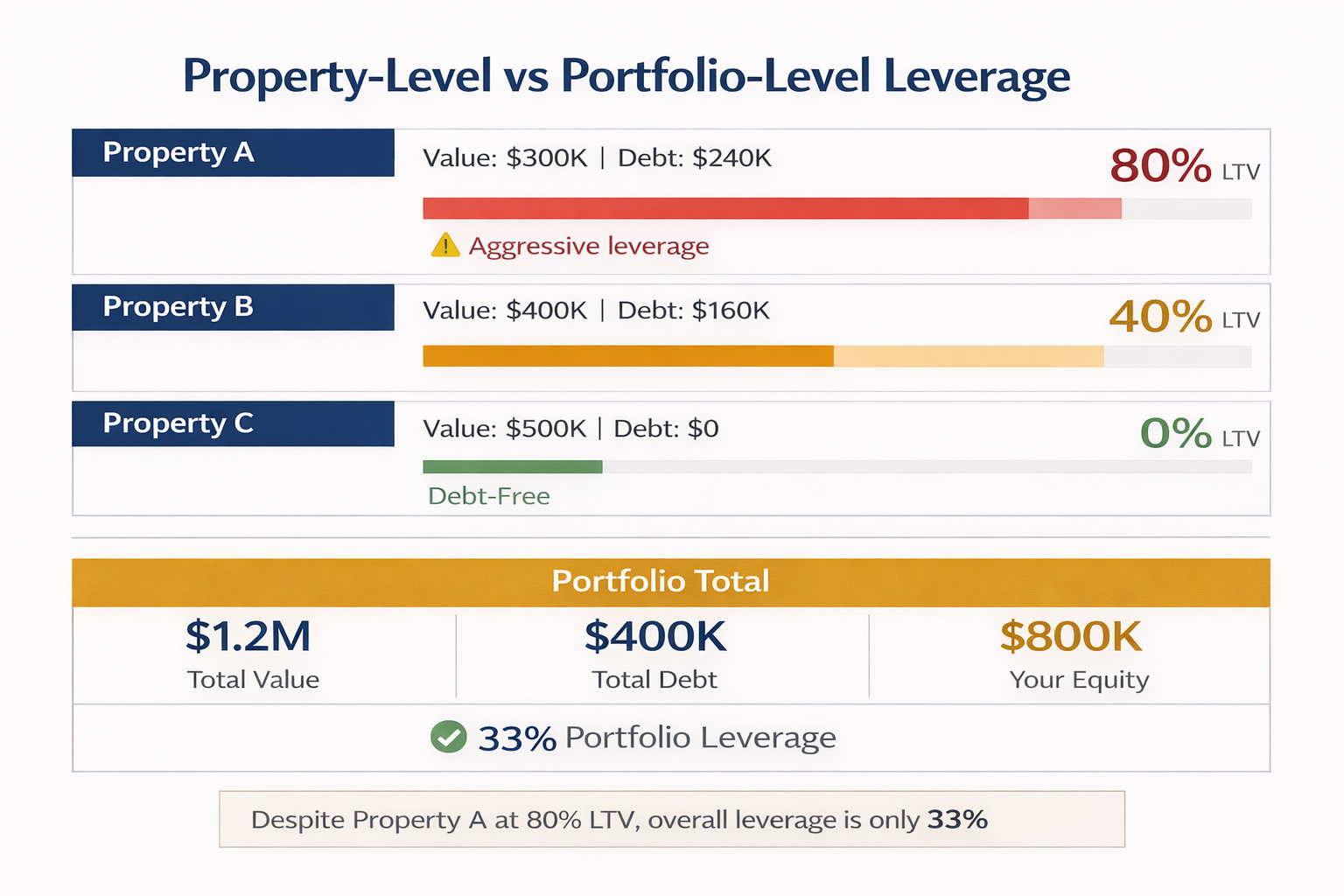

- Track Property A: $300k value, $240k debt (80% LTV)

- Track Property B: $400k value, $160k debt (40% LTV)

- Track Property C: $500k value, $0 debt (0% LTV)

They look at Property A and think: "That's aggressive."

They look at Property C and think: "That's safe."

But portfolio-wide?

Total value: $1.2M Total debt: $400k Portfolio leverage: 33%

That's actually quite conservative - even with one property at 80% LTV.

And then what?

This changes your risk assessment completely. One highly leveraged property in an otherwise conservative portfolio isn't dangerous. It's strategic deployment of debt where it makes sense.

But you can't see this if you only look at properties individually.

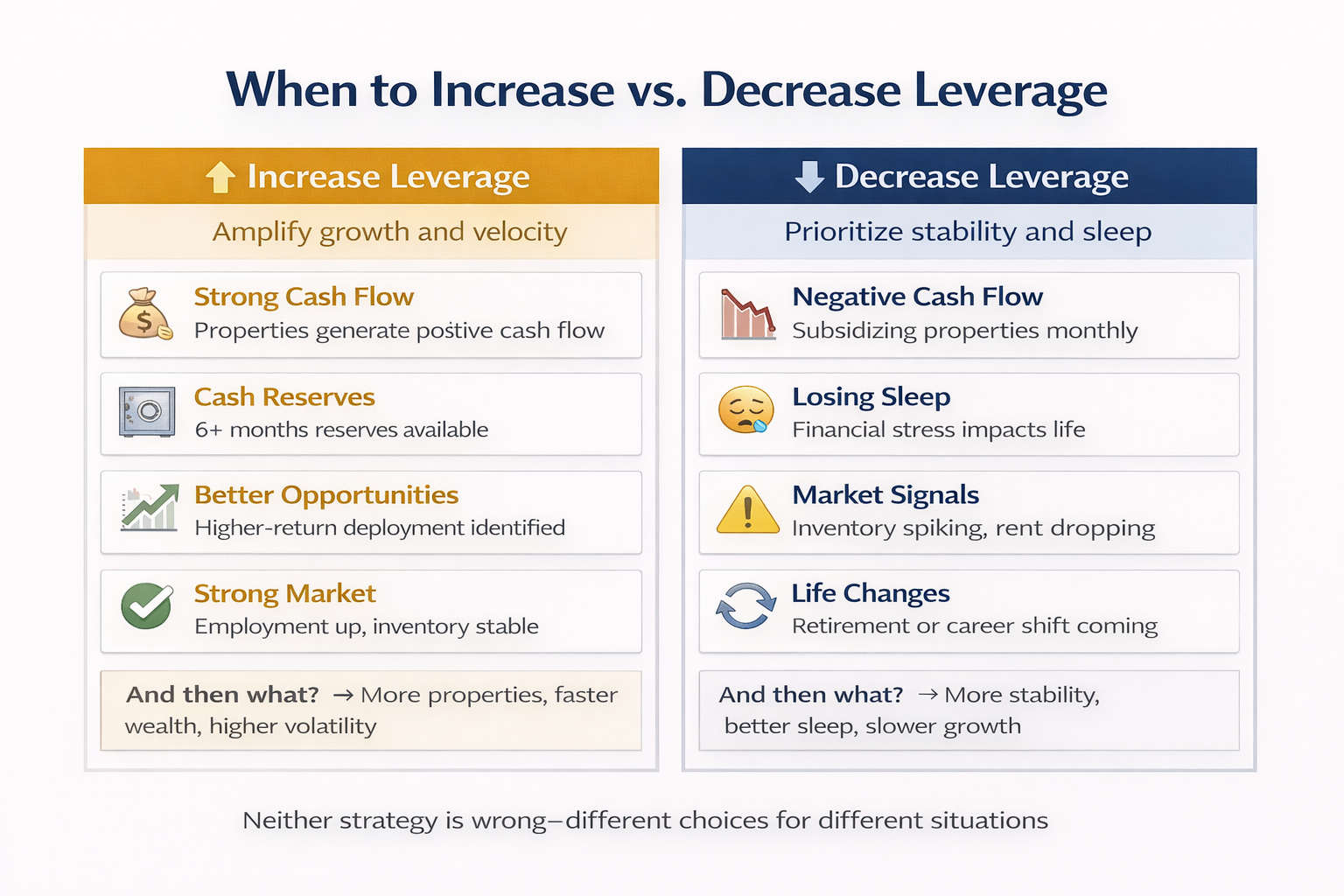

When To Increase Leverage (And When To Run Away From It)

The "right" leverage ratio depends on what happens next.

Increase leverage when:

- Your properties generate strong cash flow (debt service isn't stressing you)

- You have 6+ months cash reserves (you can survive vacancies and repairs)

- You've identified better deployment opportunities (the capital can earn more elsewhere)

- Market fundamentals are strong (employment up, inventory stable, rent growth positive)

And then what? You control more real estate with the same equity. Your wealth compounds faster. You diversify across more properties and markets.

Decrease leverage when:

- You're subsidizing properties monthly (cash flow is negative after true expenses)

- You're losing sleep (financial stress is real stress)

- Market signals are flashing red (inventory spiking, rent growth negative, job losses)

- Major life changes are coming (retirement, career shift, health issues)

And then what? You sleep better. You have more options. You can weather downturns without forced sales. You trade growth for stability.

Neither is wrong. They're different strategies for different situations.

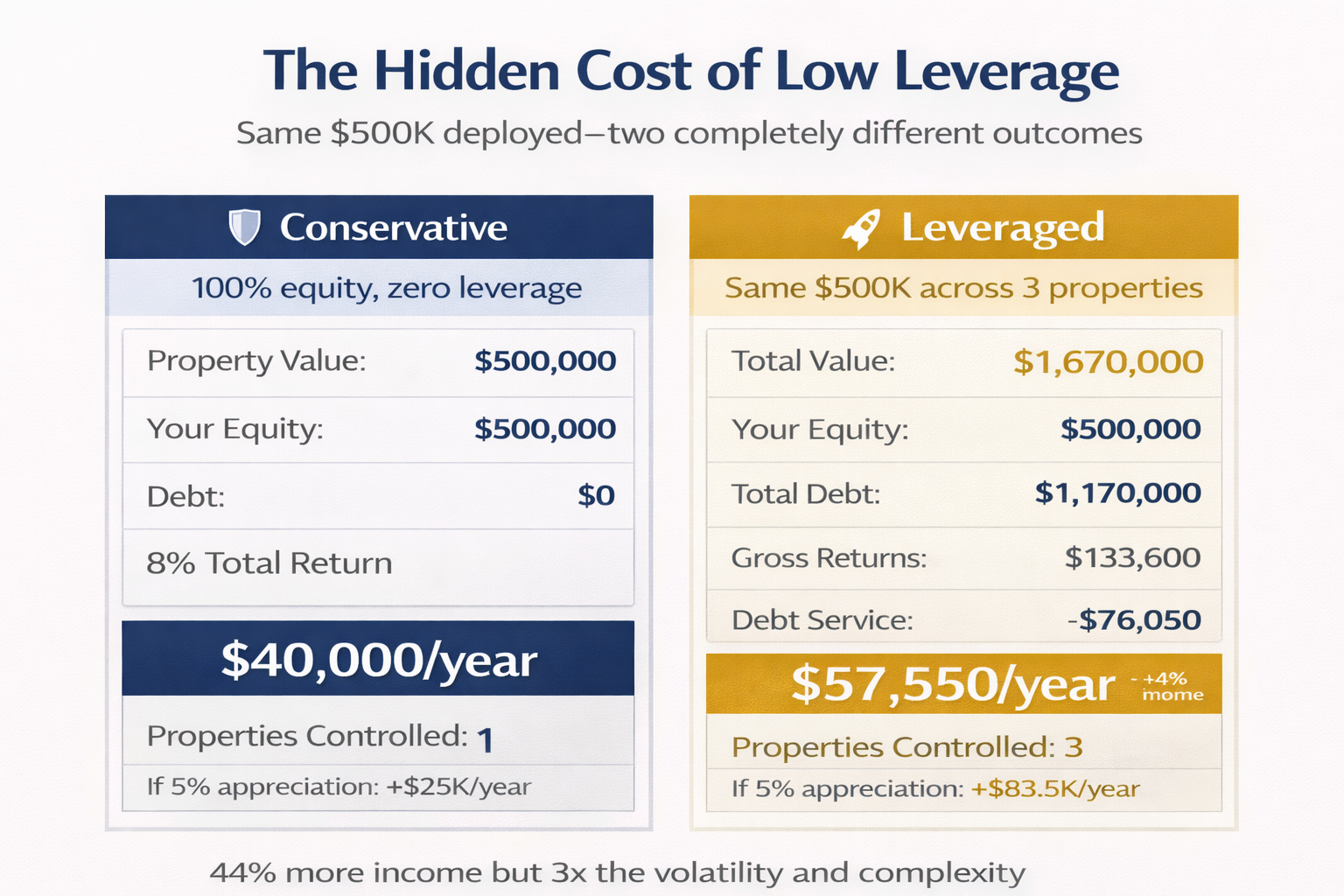

The Hidden Cost Nobody Talks About

Here's the uncomfortable truth about low leverage:

It's expensive.

Not in interest payments. In opportunity cost.

You have $500,000 sitting in a fully paid-off property earning 8% total return. That's $40,000 per year. Solid.

But what if you extracted $350,000 at 6.5% interest and deployed it into two more properties at 70% leverage?

Original property:

- Now: $500k value, $350k debt, $150k equity

- Still earning $40k/year

- Debt service: $22,750/year

- Net to you: $17,250/year on $150k equity = 11.5% return

New properties (with your $350k as down payments):

- Control: $1.17M in additional real estate

- Earning 8% total return: $93,600/year

- Debt service on $820k borrowed: $53,300/year

- Net to you: $40,300/year on $350k equity = 11.5% return

Total position:

- $57,550/year total income vs. $40,000 originally

- You're earning $17,550 more annually

- You control $1.67M in real estate instead of $500k

And then what?

If all three properties appreciate 5%, you're gaining $83,500 per year instead of $25,000. If they drop 10%, you're losing $167,000 instead of $50,000.

This is the trade-off. Higher potential returns. Higher potential losses. More complexity. More management time.

The paid-off property isn't wrong. It's just a different choice with different outcomes.

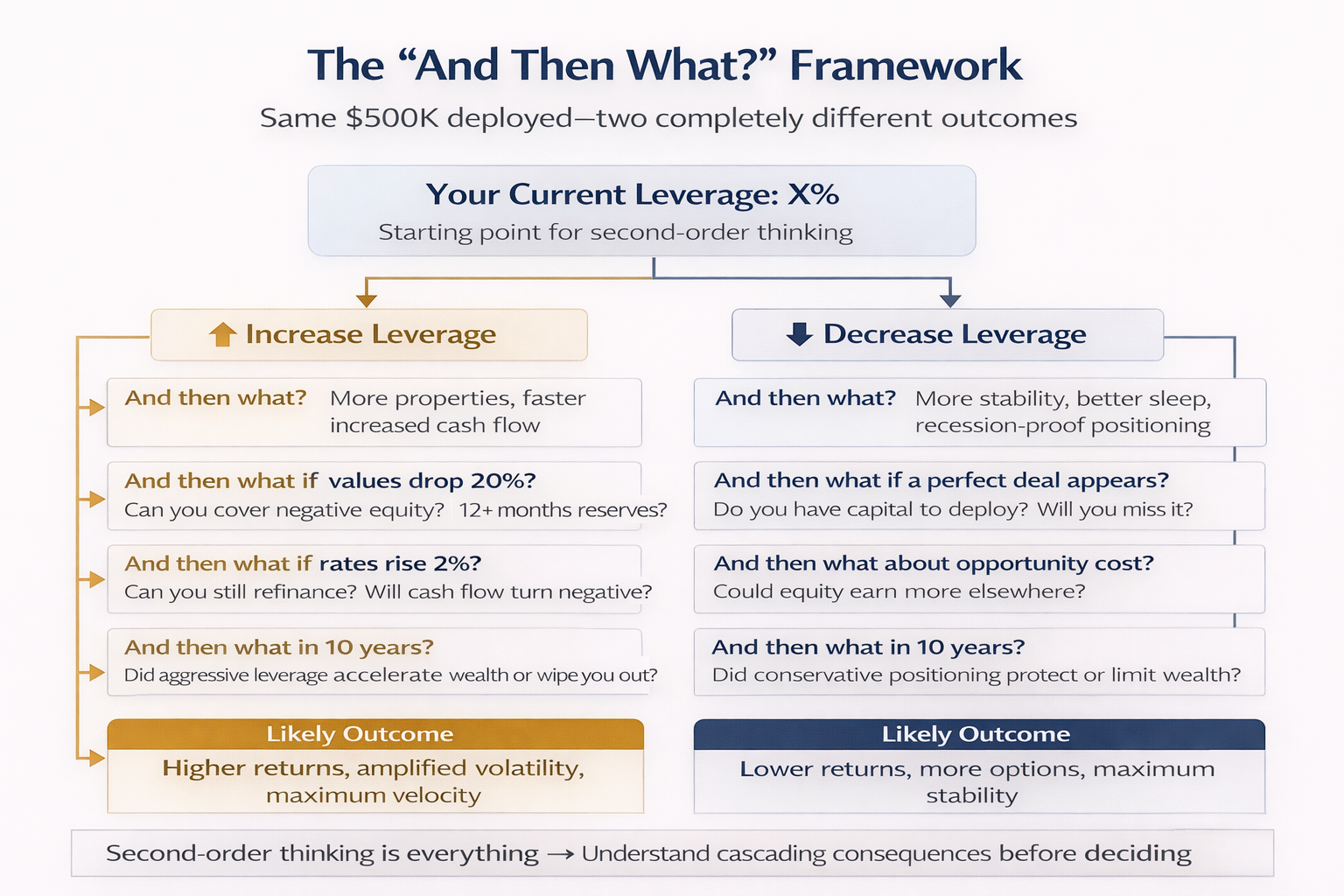

How To Know Your Number

Three steps:

1. Calculate your current leverage

Add up every mortgage balance across every property. Add up every current property value. Divide debt by value.

That's your leverage ratio.

2. Assess your comfort zone

- 30-50% leverage: Conservative (recession-proof, slower growth)

- 50-70% leverage: Moderate (balanced risk/reward)

- 70-85% leverage: Aggressive (maximum velocity, maximum vulnerability)

Where you should be depends on: age, risk tolerance, cash reserves, income stability, portfolio size, and whether you can sleep at night.

3. Ask "and then what?" for both directions

If you increase leverage:

- And then what? More properties, faster growth, more complexity

- And then what if values drop 20%? Can you survive?

- And then what if rates rise 2%? Can you refinance?

If you decrease leverage:

- And then what? More stability, slower growth, fewer opportunities

- And then what if a perfect deal appears? Do you have capital to deploy?

- And then what in 10 years? Did conservative positioning cost you wealth?

Neither path is wrong. But both have consequences worth thinking through.

The Only Number That Matters

Your leverage ratio tells you one thing with perfect clarity:

How much of your portfolio you actually own versus how much the bank owns.

It's not about good or bad debt. It's not about being "over-leveraged" or "conservative."

It's about understanding the multiplier you've chosen - and making sure that multiplier matches your goals, your risk tolerance, and your ability to handle what comes next.

Because in real estate, what comes next is rarely what you expected.

Know your number. Understand what it's amplifying. Adjust accordingly.

See your leverage ratio across every property in your portfolio → Track your portfolio intelligence with Nimbus